18 06 2015

Thursday

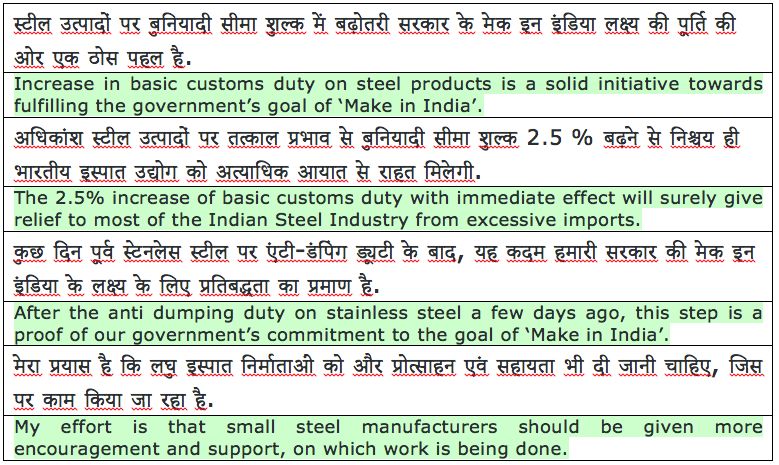

GOVERNMENT has increased the Customs duty on steel by a complicated amendment to Sl. Nos 330 and 334 in the table to Notification No. 12/2012- Customs, dated the 17th March, 2012.

The Steel Industry has welcomed the hike, as it is likely to curb the imports from China. The hike is not going to have substantial effect as imported steel is still going to be cheaper than domestic steel. And China may reduce the price thereby offsetting the duty hike for the Indian consumers.

The Steel Minister Narendra Singh Tomar tweeted:

(Disclaimer: The English translation is only for the benefit of those who don't understand Hindi. I neither claim credit, nor take responsibility for its accuracy, which you may accept at your own risk.)

Notification No.39/2015 - Customs, Dated: June 16, 2015

Amendments in NI Act come into force thru Ordinance

THE President has promulgated the Negotiable Instruments (Amendment) Ordinance, 2015.

The Negotiable Instruments Act is one of our oldest existing statutes, having been enacted in 1881. Some years ago when I was in possession of a dishonoured cheque, the first problem was to find the jurisdictional court where I could file the complaint under Section 138 of the NI Act.

The Supreme Court in a major decision last year held that once the cause of action accrues to the complainant, the jurisdiction of the Court to try the case would be determined by reference to the place where the cheque is dishonoured.

Pursuant to the judgment of the Supreme Court, representations have been made to the Government by various stakeholders, including industry associations and financial institutions, expressing concerns about the wide impact this judgment would have on the business interests as:

1. it will offer undue protection to defaulters at the expense of the aggrieved complainant;

2. it will give a complete go-by to the practice /concept of 'Payable at Par cheques' and would ignore the current realities of cheque clearing with the introduction of CTS (Cheque Truncation System) where cheque clearance happens only through scanned image in electronic form and cheques are not physically required to be presented to the issuing branch (drawee bank branch) but are settled between the service branches of the drawee and payee banks;

3. it will give rise to multiplicity of cases covering several cheques drawn on bank(s) at different places; and

4. adhering to it is impracticable for a single window agency with customers spread all over India.

To address the difficulties faced by the payee or the lender of the money in filing the case under section 138 of the Act, because of which, large number of cases are stuck, the jurisdiction for offence under section 138 has been now clearly defined.

The Negotiable Instruments (Amendment) Ordinance, 2015 provides for the following, namely:-

1. Trial of cases only by a court within whose local jurisdiction the bank branch of the payee, where the payee presents the cheque for payment, is situated;

2. Stipulating that where a complaint has been filed against the drawer of a cheque in the court having jurisdiction under the new scheme of jurisdiction, all subsequent complaints arising out of section 138 of the said Act against the same drawer shall be filed before the same court, irrespective of whether those cheques were presented for payment within the territorial jurisdiction of that court;

3. Stipulating that if more than one prosecution is filed against the same drawer of cheques before different courts, upon the said fact having been brought to the notice of the court, the court shall transfer the case to the court having jurisdiction as per the new scheme of jurisdiction; and

4. Amending Explanation I under section 6 of the said Act relating to the meaning of expression "a cheque in the electronic form", as the said meaning is found to be deficient because it presumes drawing of a physical cheque, which is not the objective in preparing "a cheque in the electronic form" and inserting a new Explanation III in the said section giving reference of the expressions contained in the Information Technology Act, 2000.

The Government expects that the amendments to the Negotiable Instruments Act, 1881 would help in ensuring that a fair trial of cases under section 138 of the said Act is conducted keeping in view the interests of the complainant by clarifying the territorial jurisdiction for trying the cases for dishonour of cheques.

And as the President is satisfied that circumstances exist which render it necessary for him to take immediate action, he has promulgated the Ordinance.

Negotiable Instruments (Amendment) Ordinance, 2015., Dated: June 15, 2015

Revenue tells Tribunal its order is perverse - Tribunal sagely tolerates

THE arrogance of the babu knows no bounds.

In an appeal memo, the Revenue pleaded that the finding of the Tribunal (in a decision followed by the Appellate Commissioner) is improper, erroneous, invalid, illegal and perverse since the same suffers from mis-consideration of the provisions of the Rule as well as misconstruing the relevant circulars issued in this behalf.

See the audacity of the babu! He is sitting in judgement on the quality of the order passed by the tribunal!

The Tribunal in sagely stature observed, "using of such language in their memo of appeal against an order of the Tribunal is not called for and the proper course available to the Revenue is to challenge the orders of the Tribunal before the higher appellate forums instead of criticizing the said orders by using improper language."

The Department did, but the Supreme Court dismissed its appeal and the perverse order of the Tribunal has attained finality.

It is not known whether the learned Revenue officers who prepared the appeal memo were aware of the fact that the order of the tribunal was confirmed by the highest court in the country. If they were, they are indirectly calling the order of the Supreme Court also as perverse. And this perverse behavior of the babus would certainly amount to contempt of the Supreme Court.

Please see Commissioner of Central Excise Vs Vijayalaxmi Gears - 2015-TIOL-1137-CESTAT-BANG

Service Tax - Commercial Training or Coaching services - 240 Cr Demand consigned to Limitation

AS reported in these columns yesterday, the huge demand by the Service Tax department on an educational institution, was set aside by CESTAT by majority on the ground of limitation.

The issue was the taxability of the appellant's service of providing coaching for engineering and medical admission tests, along with the regular intermediate course. The CESTAT by majority held that such coaching is liable to Service Tax under "commercial training or coaching". The tribunal also by majority held that the demand was time barred.

On the issue of limitation, the Members made some interesting observations.

Member (T):

- If the submissions made by the learned counsel are accepted, if a tax payer takes a stand that he is not liable to pay even after being informed on some ground or the other the moment department writes a letter to him, the limitation clock starts striking and within one year if the show-cause notice is not issued, no extended period could be invoked for the demand.

- If this claim is accepted, persons who defy the law and law enforcement agency and avoid complying with the directions and requests and force the department to undertake coercive measures would be better off than a law abiding citizen who likes to pursue the matter in a legal and proper manner.

- Question arises then what would be legal and proper procedure for doing this. If a law abiding citizen would have taken the registration and filed the returns with the relevant information showing the service tax payable but would not have paid the same if he really felt he would not be liable to pay. This is the proper legal course to adopt which would mean that there is no suppression of facts on the part of the assessee since the information required has been given and the self-assessment procedure, which is the procedure at present adopted under service tax matters has been followed.

- When an assessee files returns showing the service tax payable but does not pay the same and he has a bona fide belief that he does not have to pay and gives a covering letter with the same, the department is bound to issue a show-cause notice within the normal period and i.e. the time when the bona fide belief would come into play since the appellant has complied with the legal requirements. This was the proper procedure which was to be followed by the assessee, if they were intending to claim that no extended period was invokable.

- On the contrary, departmental officers also could have entertained a belief that in any case they have 5 years' time for issuing the show-cause notice since the appellant has defied the law and was not cooperating and was not providing the information and was not following the law by taking registration and filing returns.

- Naturally the departmental officers after requesting the assessee for two years proceeded to conduct search operations, investigation, recovery of records and issue of show-cause notice.

- There has to be some difference between a person who tries to abide with the law, and tries to cooperate and tires to ensure that he understands the law and implements the same and another person who simply takes a stand and goes on putting hurdles and goes on corresponding without proceeding to undertake actions in accordance with law which is required of him.

- The claim of the appellant that extended period is not invokable because the information was not called for and therefore they had not violated any provisions is not at all acceptable.

- It is also to be taken note of that service tax is an indirect tax and all that the appellants had to do was to charge service tax to the students and pay it to the government. Unlike several cases that come before us day in and day out wherein department would have issued show cause notice after a number of years imposing liability to tax which would not have been collected but would have to be paid with interest besides suffering penalty, this is a case where department informed the appellants within 15 days of service tax imposition on the activity.

- If an assessee has to plead a bona fide belief, such a bona fide belief has to be pleaded during the relevant time and not on the basis of subsequent decisions. In this case, when the assessee intimated the department that assessee being a charitable trust was not liable to service tax, there were no decisions of any judicial forum taking such a view. Such decisions came only in 2008 and thereafter.

Member (J):

- Delay in furnishing information sought for by Revenue from the appellant, cannot be a ground for invocation of extended period.

- All the powers of a Court with regard to attendance of witness, discovery of information/documents, etc. are vested in the adjudicating authority.

- Only for failure on the part of the adjudicating authority to exercise jurisdiction vested in him, extended period is not invokable.

The Third Member (also Judicial)

- The Appellant took a plea that it is a charitable institute and not covered within the definition of "Commercial Training or Coaching Centre". It is true that this view was supported by the catena decisions of the Tribunal. But, this was resolved against the Appellant by inserting Explanation under Section 65(105)(zzc) of Act, with retrospective amendment by Finance Act, 2010 that the expression "Commercial Training or Coaching Centre" shall include a Trust or a Society with or without profit motive. So, the finding of the Adjudicating Authority that the Appellant tried to mislead the department by stating that their committee is non-commercial nature with an intention to evade payment of tax, cannot be accepted.

- It cannot be said that there was a suppression of facts with intent to evade payment tax.

- In any event, the difference of opinion on the leviability of Service Tax in the present case would also support the bonafide belief of the Appellant of the leviability of tax.

- I agree with the order of learned Member (Judicial) and the demand of tax is barred by limitation.

We bring you this huge (in length and amount of demand) judgement today. Please see Breaking News.

WCO Photo Competition 2015 - The Austrian Entry

Until Tomorrow with more DDT

Have a nice day.

Mail your comments to vijaywrite@tiol.in |

Download PDF

Download PDF