Untitled Document

|

TIOL's News |

| |

In DDT 2962, while highlighting the collateral damage caused while granting Service Tax largesse to the aforesaid endeavour of the government - UDAN - "Ude Deshka Aam Nagrik", we had mentioned - While granting exemption to air passengers, CBEC by mistake withdraws Cenvat credit on input services for renting of hotels.

What had actually happened is best explained by extracting the following table.

Kindly Note - In between the entries 5 and 6 to the notification 26/2012-ST, an entry 5A was inserted by the amending notification 38/2016-ST dated 30.08.2016 resulting in the following -

| Sl.No. |

Description of taxable service |

Percentage |

Conditions |

| (1) |

(2) |

(3) |

(4) |

| 5 |

Transport of passengers by air, with or without accompanied belongings in

(i) economy class

(ii) other than economy class |

40

60 |

CENVAT credit on inputs and capital goods, used for providing the taxable service, has not been taken under the provisions of the CENVAT Credit Rules, 2004. |

| 5A. |

Transport of passengers, with or without accompanied belongings, by air, embarking from or terminating in a Regional Connectivity Scheme Airport. |

10 |

CENVAT credit on inputs, capital goods and input services, used for providing the taxable service, has not been taken by the service provider under the provisions of the CENVAT Credit Rules, 2004. |

| 6 |

Renting of hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes. |

60 |

Same as above |

Inasmuch as whereas the condition attached to serial no. 6 above prior to insertion of Serial no. 5A was non-availment of CENVAT credit on Inputs and Capital goods, consequent upon the insertion of Serial no. 5A the condition has enlarged itself to mandate non-availment of CENVAT credit on Inputs, Capital Goods and Input Services.

DDT also said -

+ Even before the Aam Nagrik has taken to the skies, the hospitality sector is already in the pit!

+ Hopefully, the CBEC realises this gaffe and extinguishes the flames before they spread far and wide. |

|

GOVERNMENT's

Response |

| |

Our sincere plea has been accepted by the responsive CBEC and that too within a week.

Yesterday, a corrigendum was issued to the notification 38/2016-ST and which does the following -

(i) in line 23, for "5" read "6";?

(ii) in the TABLE, in column 1, for "5A" read "6A";?

(iii) in line 31, for "5A of the TABLE" read "6A of the TABLE".

Read DDT 2969 dated: 11-11-2016 for details

|

|

TIOL's News |

| |

In DDT

2819 published: April 04, 2016

Responsive Board - DDT Effect - Board amends |

| |

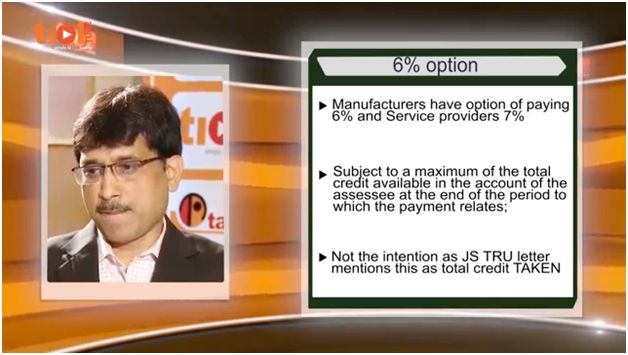

TIOL TUBE Discussed:

Budget 2016 introduced several assessee-friendly amendments in Rule 6 of the CCRs, 2004. However, there was one anomaly in the amended Rule. Not many observed this in fine print, but during Post-Budget Analysis, we raised this issue and pointed out that the Rule has not been properly drafted to reflect the intention of the Government.

|

| |

|

|

GOVERNMENT's Response |

| |

Now, the responsive Board has done the needful. An amendment has been made to sub-rule (3) of Rule 6. The amended Rule reads:

(i) pay an amount equal to six per cent. of value of the exempted goods and seven per cent. of value of the exempted services subject to a maximum of the sum total of opening balance of the credit of input and input services available at the beginning of the period to which the payment relates and the credit of input and input services taken during that period; or�;

As per this amended provision, assuming during a month, the value of exempted goods to be Rs one crore, the 6% amount would be Rs 6,00,000/-. However, if the opening balance of the credit of input and input Services plus the credit taken on all inputs and input Services during that month is Rs 1,20,000/- only, then the 6% amount would be restricted to Rs 1,20,000/- only.

All is fine, but even this new amendment has a problem. While Table No 6 of the ER1 return (CENVAT statement) has separate columns for fresh credit of inputs, input services and Capital goods, the opening balance of credit at the beginning of the Month does not have item-wise break up. This means, the opening balance of Credit includes capital goods credit and it is not possible to identify the �opening balance of credit on inputs and input services available� for the purpose of Rule 6(3).

Perhaps it is not easy to solve the problems created by this Rule which was born as Rule 57CC with several congenital defects. Even the surgery performed in 2016 budget seems to have side effects. |

| |

|

|

TIOL's News |

| |

In DDT

2766 published:

January 15, 2016

TIOL Effect - CBEC Corrects Exchange Rate Notification - DDT Effect - Board amends |

| |

|

|

TIOL's News |

| |

|

| |

|

|

TIOL's News |

| |

In DDT 2646 published: July 22, 2015 Confusing, Complicated and Controversial Notifications - Storm in the Teacup blows over - DDT Effect - Board amends

|

|

TIOL's News |

| |

Setting the Cat amongst the Pigeons Published: July 21, 2015 |

| |

Notification No. 34/2015-CE causes mighty problems for Notfn. 30/2004-CE Published: July 21, 2015 |

| |

Carelessness in drafting notifications Published: July 21, 2015 |

| |

Is it a mini budget or a step towards GST? Published: July 21, 2015 |

| |

|

|

GOVERNMENT's Response |

| |

The Central Government had issued notifications No 34, 35 & 36/2015-CE and goofed up the entire scheme of concessional duty offered for 'Make in India' Scheme. After TIOL and its Netizens quickly pointed out the mistakes in drafting and the intent, the Government was quick to amend them by issuing Notifications No 37, 38, 39-CE, all dated 21.07.2015 setting right its Confusing, Complicated and Controversial Notifications. |

| |

|

|

TIOL's News |

| |

In Cob(Web) - 323 published on DECEMBER 20, 2012, titled Dear FM, it is time now to get serious about Directorate of Taxpayers' Services |

|

TIOL's News |

| |

In DDT -

2499 published on

DECEMBER 18, 2014 , DDT reported the CBEC faux pas in overvaluing the exchange rate of Japanese YEN by a hundred times. |

|

GOVERNMENT's

Response |

| |

The Board was quick to act and in a day's time itself they rectified the mistake by issuing a corrigendum. DDT reported about the correction being done in DDT - 2500. |

|

TIOL's News |

| |

In Cob(Web) -

419 published on

OCTOBER 23, 2014 , titled 'Rising NPAs - Fault lies with our lax Regulator!' + Mixed Buzz published on

OCTOBER 28, 2014, titled Govt disbands PSBs; sets up Panel to select CMDs for Public Sector Banks. In Cob(Web)

- 151 published on September 3, 2009, titled 'New

contours of modern Indian economy: Has Revenue Secretary's post indeed

become redundant? - Part III' and in Cob(Web)

- 152 titled "Dear

FM, it's time to merge CBDT & CBEC, and create a Council for

Revenue Management as policy catalyst!" published

on September 10, 2009, TIOL talked about scrapping of the post of Revenue

Secretary and setting up of a Tax Council to take care of the legislative

activities. |

|

GOVERNMENT's

Response |

| |

In

its First Report, the Tax Administration Reform Commission (TARC),

headed by Dr Parthasarthy Shome, has called for scrapping of not only

the post of Revenue Secretary but also the liquidation of Revenue Hqs

and their functions can be distributed among both the Boards. The Commission

has also called for elevating the post of Chairman in the Revenue Boards

to the level of Secretary to the Union Government and the Boards must

be given financial autonomy. The TARC has also called up a Tax Council

model to make the system more efficient.

The Shome Commission has to say: "... the post of Revenue Secretary does not merit presence in a modern tax administration. Instead, a Governing Council should be introduced with the chairs of the Boards alternating as its chairperson ... and the Council should include members from the non-government sector as well. The Governing Council will oversee the functioning of the two Boards and approve broad strategies ..."

TIOL is thankful to the Commission for finding substance in our views and giving it due place in its Report with some extra details relating to who should head this Council and developing TPL and TRU as a powerhouse of researched fiscal wisdom. |

|

TIOL's News |

| |

NOTIFICATION 26/2012-ST

dated 20.06.2012 provided abatement of 75% and 70% to two different

groups of residential complexes / units. In DDT

2064 13.03.2013, while reporting a Netizen's dilemma, it was mentioned:

"English Vinglish: Service Tax - Abatement - Construction of Residential Unit - Confusion between FM's Speech and CBEC Notification

DDT added: The notification clearly failed to give effect to the intention of the Government reflected in the Budget speech of FM. The Notification in the present form allows 75% abatement to a flat having a carpet area of 1000 sft and costing Rs 2 crores. Actually, in such cases, the abatement should have been only 70%, if we go by the Budget Speech. The Notification reads now:

12. |

Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly except where entire consideration is received after issuance of completion certificate by the competent authority,- |

|

(i) CENVAT credit on inputs used for providing the taxable service has not been taken under the provisions of the CENVAT Credit Rules, 2004;

(ii) The value of land is included in the amount charged from the service receiver |

(i) for residential unit having carpet area upto 2000 square feet or where the amount charged is less than rupees one crore; |

25 |

|

(ii) for other than the (i) above |

30 |

|

Perhaps, it should have been worded like this:

12. |

Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly except where entire consideration is received after issuance of completion certificate by the competent authority,- |

|

(i) CENVAT credit on inputs used for providing the taxable service has not been taken under the provisions of the CENVAT Credit Rules, 2004;

(ii) The value of land is included in the amount charged from the service receiver. |

|

|

(i) for residential unit having carpet area of 2000 square feet or more OR where the amount charged is more than rupees one crore; |

30 |

|

|

|

(ii) for other than the (i) above. |

25 |

|

�

|

|

GOVERNMENT's Response |

| |

After nearly two months, the Central government has corrected this fiasco.

By an amending Notification, the entry referred above has been substituted thus -

"12. |

Construction of a complex, building, civil structure or a part thereof, intended for a sale to a buyer, wholly or partly, except where entire consideration is received after issuance of completion certificate by the competent authority,-

(a) for a residential unit satisfying both the following conditions, namely:-

(i) the carpet area of the unit is less than 2000 square feet; and

(ii) the amount charged for the unit is less than rupees one crore;

(b) for other than the (a) above.

|

25

30 |

(i) CENVAT credit on inputs used for providing the taxable service has not been taken under the provisions of the CENVAT Credit Rules, 2004;

(ii) The value of land is included in the amount charged from the service receiver.". |

Notification 9/2013-ST dated 8 th May, 2013

|

|

TIOL's News |

| |

No Education Cess from 01-07-2012!

On June 26, 2012 TIOL published the above article in its DDT column. |

| |

No More Cess from July 1, 2012?

On June 26, 2012 TIOL published the above article in its

SERVICE TAX - NEW LAW +VE or -VE

column. |

|

GOVERNMENT's Response |

| |

Circular No 160/2012, Dated : June 29, 2012

Levy of Education Cess on Service tax from july 1, 2012: CBEC takes help of General Clauses Act, 1897 to retrieve lost ground |

| |

Order No 2/2012, Dated: June 29, 2012

CBEC Order on levy of education cess from July 1, 2012 |

|

TIOL's News |

| |

Boiler Credit - CBEC Responds

BY Circular No. 964/07/2012-CX dated 02.04.2012, Board made some very important clarifications.

"structural components which are to be used essentially as a part of Boiler System would be classifiable as parts of Boiler only under Heading 8402 of the Tariff. It is further clarified that since these structural components are nothing but the parts and accessories of the Boiler, they would be covered by the definition of inputs under Rule 2(k)(iii) of the CENVAT Credit rules, 2004 (i.e. all goods for generation of electricity & steam)."

DDT did not make any adverse comments on this circular, when it was carried in DDT 1830 � 04.04.2012; in fact, we mentioned, "This is a beneficial clarification and let us hope the pending disputes would be settled".

In DDT 1831 - 09.04.2012, we asked a question whether this clarification would apply to goods 'other than' boilers?

Board issued another Circular - 966/09/ 2012-CX, Dated: May 18, 2012, in which it was clarified that while CENVAT Credit is available in respect of parts of Boiler, the same is not admissible in respect of the structural components used for laying of foundation or making of structures for support of capital goods/ Boiler.

While reporting this in DDT 1861 - 21.05.2012, DDT observed, "It is beyond reason, why the Board should create so much confusion by issuing circulars. Can't they just be satisfied with their confusing rules and notifications? Should they complicate matters further by issuing clarifications on which further clarifications have to be issued within less than two months ?"

The CBEC responded pretty fast. Member (CX) in CBEC, Sreela Ghosh, spoke to DDT expressing her anguish at the harsh criticism, but patiently explained the need for the second circular.

The Director (CX) in the Board clarified the position as:

The relevant facts leading to the issuance of the circular no 964/07/2012-CX dated 2nd April 2012 are as follows:

++ The manufacturer of Boiler, clears the Boiler and it components/ parts/accessories after classifying them under tariff heading 8402 and pays the duty accordingly.

++ Amongst the parts cleared there are certain components which are used for construction of support to the Boiler. These too are classified by the Boiler manufacturer under the same heading.

++ The jurisdictional officers from where the Boiler and its parts/ components are being cleared are in agreement with the classification made.

++ However the officers in the jurisdiction where the CENVAT credit is being taken by the recipient of the Boiler and its parts, have been raising the issue with regard to the admissibility of CENVAT credit in respect of the certain components. The argument advanced by these officers is that since these structural components are not contributing to the functioning of the Boiler but are used for manufacture of supporting structure in respect of the Boiler, therefore they will be hit by the exclusion clause in the definition of input, read along with the decision of the tribunal in case of the Vandana Global [2010 �TIOL-624-CESTAT-DEL-LB]

After examination of the issue in consultation with the jurisdictional officers, the Board clarified that only those structural components which are essential for manufacture of the Boiler and are necessary for its operation shall merit classification under heading 8402. It was also clarified that since these structural components are essential to the functioning of the Boiler they shall be eligible for CENVAT Credit. The natural corollary to the assertion made is that those structural components which only provide support to the boiler (e.g. those used for laying foundation) will not be classifiable under heading 8402. Further as these structural components are used for construction of support to the Boiler the CENVAT credit shall not be admissible in respect of these items.

After issue of the Board circular dated 2 nd April 2012, certain doubts were expressed with regard to the scope of the clarification issued in the said circular. Accordingly a second circular vide 966/09/2012-CX dated 18th May 2012 was issued reiterating the position and indicating that admissibility of CENVAT credit on structural components used for construction of support to the Boiler are in accordance with the judicial pronouncements on the subject.

With regard to the issue of jurisdiction mentioned in the Article, it may be mentioned that it is a well settled law that goods are to be classified in the jurisdiction where they are manufactured and cleared and the jurisdiction in which they are received cannot alter the classification of the goods. The circulars in question do not attempt to clarify issue of the jurisdiction.

We are grateful to the Board for its prompt response and clarification. So, the position now is that structural components essential to the functioning of the Boiler are eligible for CENVAT Credit and classification of the product is not to be done at the receiving end. There can be absolutely no dispute with this view of the Board.

A responsive tax administration commands respect and confidence. |

|

TIOL's

News |

| |

1% Duty Goods - Now Entitled to Filing Quarterly Returns - Board Corrects error pointed out by DDT

In DDT 1830 – 04-04-2012, we pointed out;

According to (the fourth) proviso in Rule 12 of the Central Excise Rules, 2002,

Provided also that, where an assessee is availing the exemption notification of the Government of India, Ministry of Finance (Department of Revenue) No. 1/2011- Central Excise, dated the 1st March, 2011, published in the Gazette of India, Extraordinary, Part-II, section 3, sub-section (i) vide number G.S.R. 116(E) dated the 1st March, 2011 and does not manufacture any other excisable goods other than those specified in the said notification, he shall file a quarterly return in the form specified by notification by the Board, of production and removal of goods and other relevant particulars, within ten days after the close of the quarter to which the return relates.

Now that certain items like coal and fertilizers are covered under Notification No 12/2012 CE, the above proviso requires amendment. Last week they corrected the CENVAT Credit Rules, 2004, but they failed to notice that Central Excise Rules also require a correction. |

|

GOVERNMENT's

Response |

| |

It took the Board just a fortnight to correct this mistake. The Proviso has been amended to provide for quarterly return for the 1% duty items covered under Notification No. 12/2012. We thank the Board for the quick response, thereby avoiding unwanted litigation and trouble. It does not give us any pleasure in pointing out the mistakes of the babus, though some of them get very angry; but it does give us tremendous happiness when Board realizes its mistakes and carry out corrections.

Notification No. 23/2012 - CX., (N.T.), Dated: April 18, 2012 |

|

TIOL's

News |

| |

PLEASE refer to DDT 1476–28.10.2010 , wherein we pointed out that Notification No. 26/2010 – Service Tax dated 22.06.2010, was issued under the wrong Section. We had pointed out that the Notification was issued under clause (aa) of sub-section (2) of section 94 while it should have been issued under Section 93(1) of the Finance Act.

Notification No. 26/2010 – Service Tax Dated June 22, 2010 reads as:

In exercise of the powers conferred by clause (aa) of sub-section (2) of section 94 of the Finance Act, 1994 (32 of 1994) (hereinafter referred to as the Finance Act), the Central Government, on being satisfied that it is necessary in the public interest so to do, hereby exempts the services referred to in clause (zzzo) of sub-section (105) of section 65 of Finance Act, 1994 from so much of service tax as is in excess of,-

(a) ten percent of the gross value of the ticket or rupees one hundred per journey, whichever is less, for passengers travelling in any class, within India;

(b) ten percent of the gross value of the ticket or rupees five hundred per journey, whichever is less, for passengers embarking in India for an international journey in economy class:

Provided that this exemption shall not apply xxxxxxxxxxxxxxxxxxxxxxxxxxxxx

For a recap, Section 94 empowers the Government to make Rules, while Section 93 empowers the Government to issue exemption Notifications.

DDT asked, “Will CBEC make a correction before some Tribunal Bench holds the notification as invalid as issued under a wrong Section of the ACT?”

|

|

GOVERNMENT's

Response |

| |

We are happy to report that the Government has realised the mistake and issued a corrigendum. The Corrigendum reads as,

“for “clause (aa) of sub-section (2) of section 94”, read “sub-section (1) of section 93 read with clause (aa) of sub-section (2) of section 94”.

Now why to read clause (aa) of sub-section (2) of section 94 ? This clause empowers the Government to make rules for determination of amount and value of taxable service. This was an exemption notification and there was no Rules Notified.

Will the Board issue another corrigendum? It is really unfortunate that notifications are issued so callously.

CBEC Corrigendum, Dated 23.11.2010 |

|

TIOL's

News |

| |

Custodial Death in Malda Customs – NATIONAL HUMAN RIGHTS COMMISSION awards interim relief of One Lakh Rupees based on TIOL Reports

Please refer to our stories:

Malda custodial death : FM finds gaping holes in internal report & orders independent probe

Kolkata Customs Custodial Death - FM deprecates TIOL-DDT 255

WE had reported about the sad story of a young man who died in the custody of the Customs. This man was selected by the Staff Selection Commission for appointment as Inspector in the very Department. Unknown to us, the National Human Rights Commission had taken up the matter based on our reports and issued a Notice to the Revenue Department.

The Revenue replied that,

No FIR has been lodged against Custom officers nor there is any evidence regarding torture or harassment by Custom officers during custody of the deceased, and therefore, Custom officers cannot be held responsible for the un-natural death of the deceased.

The Govt. after getting proper inquiry conducted in the matter has issued Warning' to the concerned officials as they were found having acted in a negligent manner and failing to provide safe custody to the deceased, and not on account of any harassment or torture in custody to the deceased. Nothing has been established on record to prove any malafide on their part. As such, there is no ground to indicate that the concerned officials violated the human rights of the deceased in any manner.

|

|

GOVERNMENT's

Response |

| |

The Commission did not agree and observed,

It is a clear case of violation of human rights of the deceased who was a young man of 30 years and died in the state custody. Secretary, Deptt. of Revenue, Ministry of Finance, Govt. of India is recommended to pay compensation of Rs. 1,00,000/- (Rupees One Lakh only) to the next of kin of the deceased as damages /interim, relief u/s 18(a)(i) of the Protection of Human Rights Act, 1993. The proof of payment be sent to the Commission within six weeks.

The Commission's Registry very kindly sent us a copy of the Order recommending compensation in Case No. : 400/25/2005-2006 .

It is a great reward for all of us in TIOL that due to our efforts, some small compensation is awarded to the poor father who lost his precious son. We hope the Revenue Department will pay up this small compensation without further prolonging the litigation. |

|

TIOL's News |

| |

ANYBODY who deals in export and import of goods, is bound to be familiar with one IT term - EDI (the Electronic Data Interchange) which CBEC is very proud of. EDI is the epicentre around which all Customs-related activities revolve today. Filing of bill of entry or shipping bill or drawback claims or refund - you name the activity, and the EDI comes into the picture. There are different cells which handle different sets of these customs works. This entails allotment of password to officials working there. And, going by the IT Security Protocol, the onus to maintain the secrecy of the password lies with individual officers. However, how careless and perfunctory these officials can afford to be, is a common site in virtually all Customs ports and Custom Houses across the country. A visitor from the private sector who visits the clearance zone and understands the deleterious fall-out of sharing of password gets horrified when he sees how office boys of CHAs use the Customs officials' passwords to the EDI at their own will. None cares as long as a fraud is not reported, and the lucre keeps swelling in concealed pockets of these officials, collecting a 'cut' for such quick facilitation of cargo!

Yet another EDI-based drawback fraud detected; CBEC suspends 31 officers but none from Group 'A' so far!

|

|

GOVERNMENT's Response |

| |

Frauds resulting from failure to maintain password security - reg Instruction |

|

TIOL's

News |

| |

In our post-budget analysis, we carried an article highlighting the

errors in Rule 6, titled ABC of Rule 6 - What is "P"? and suggested

an amendment.

|

|

GOVERNMENT's

Response |

| |

We are happy to report that the necessary amendment has been made to

this Rule vide Corrigendum issued. |

|

TIOL's

News |

| |

|

|

GOVERNMENT's

Response |

| |

| Now

part of Finance Bill |

| 1. Explanation in Finance Bill confirms the levy on lottery/games |

| 2. Service

Tax is proposed to be levied on renting and leasing of capital assets

like crane and machineries |

| 3. Major amendment

in Rule 6 of CCRs, 2004 proposed |

| 4. Many taxes

levied on IT-related services and goods under ST & Excise |

| 5. Parity in

duty rates has been achieved |

| 6. More than

expected changes in the tax exemption slabs |

| 7. Most of the

amendments like Sec 11D + Rebate etc proposed |

| 8. Hike in threshold

limit to Rs 10 lakh for small service providers; dispute settlement scheme

in Service Tax, Amendment to deny exemption to certain so-called charitable

institutions and many more |

|

|

TIOL's

News |

| |

Nearly two years ago TIOL edit team had highlighted the practical difficulties

faced by the consignors/consignees who are liable to pay service tax on Goods

transport agency service. In order to avail the benefit of the 75% abatement,

they had to ensure that the goods transport agency did not avail cenvat credit

on the inputs or capital goods. It was suggested that the tax rate on this

service should be reduced unconditionally by extending the 75% abatement without

any strings attached. Read Story |

|

GOVERNMENT's

Response |

| |

TIOL is happy to report that in this year’s budget, Notification 13/2008 dated

1.3.2008, has been issued to extend the benefit of 75% abatement without imposing

any conditions. |

|

TIOL's

News |

| |

TIOL-DDT

621 25.05.2007, mentioned about an inadvertent omission which made

jute twine dutiable all of a sudden. Extracts from the DDT.

This

is a classic example of how unintended actions can be disastrous to the

trade and industry. Jute goods have been enjoying exemption for quite

some time and twine is no exception. To eliminate the hassles

of even exemptions, the Tariff rate itself is made NIL in the Central

Excise Tariff. But in the maze of amendments to the Central Excise Tariff

from 6 digit to 8 digit and consequential amendments to the related exemption

Notifications, a small error is now snowballing into huge demands and

going to be another gold mine for the consultants. |

|

GOVERNMENT's

Response |

| |

We

are very happy to report that the Government has very graciously understood

the problem and has stopped the big forest fire. Now they have issued

a notification whereby Twine of jute or other textile bastfibres of heading

5303, is exempted from the whole of the duty.

This

brings a lot of cheer to the harassed jute manufacturers of Kolkotta and

other places. Reports have reached us that after seeing our flash yesterday,

dancing assessees have gone to Central Excise offices and distributed

sweets.

The

CBEC deserves all praise for correcting this inadvertent lapse, but there

is another problem.

NOTIFICATION

NO. 28/2007-Cex., Dated: June 15, 2007

See

detailed report in TIOL-DDT

638 19.06.2007 |

|

TIOL's

News |

| |

In

our Budget articles, we had carried a story Amendment

to Rule 21 of CE Rules - Half done !

wherein

it was pointed out that

In

the second and third provisos, in fact two words need to be substituted

in each proviso, for upper and lower limits, but only one word of the

revised upper limit has been substituted. So now there is overlap of powers

between the Superintendent , Assistant/Deputy Commissioner and the Joint

Commissioner. Therefore there is a need to substitute " one thousand"

in second proviso to "ten thousand" and in the third proviso,

"two thousand five hundred" needs to be replaced with "one

lakh rupees". |

|

GOVERNMENT's

Response |

| |

We

are happy to report that the Government has corrected the mistake by issuing

the corrigendum below:

CORRIGENDUM

to Notification No. 8/2007 dated the 15th March, 2007 |

|

TIOL's

News |

| |

While

withdrawing many exemption notifications, the Govt also withdrew exemption

given to food preparations and waters, not cleared in sealed containers.

Water provided by municipal bodies became excisable from March 1, 2006

(See DDT

357 - 08- 05- 2006) We also pointed out even if the exemption is restored,

what about the interim period? Fortunately, the Govt has issued an 11C

notification for this. |

| |

|

|

GOVERNMENT's

Response |

| |

In

response to our remarks, the Govt has not only restored the exemption

but also issued 11C Notification, exempting it for the interim period.

SEE

DDT370 |

|

TIOL's

News |

| |

Vizag

and Mumbai notified as proper Customs ports. We had reported on several

occasions that Vizag is not an authorised port for imports and all goods

imported through Vizag are liable for confiscation and all the officers

who abetted this are liable to penal action. |

| |

|

|

GOVERNMENT's

Response |

| |

Now

Government has amended the Notification to rectify the lapse pointed out

by TIOL

SEE

the DDT370 |

|

TIOL's

News |

| |

AFTER the budget we reported on the confusion arising among taxpayers because

of the newly introduced ATM services.

SEE

the NEWS |

| |

|

|

GOVERNMENT's

Response |

| |

We

are happy to report that the Government has indeed come out with a clarification

that Service Tax is not proposed to be levied on use of cards in ATMs.

SEE

the DDT |

|

TIOL's

News |

| |

THERE were no Rules for recruitment of CBDT & CBEC Chairmen and Members. This

was, on umpteen occasions, highlighted and debated by TIOL which also suggested formation of a Selection Committee to pick up Members

on merit basis.

|

| |

|

|

GOVERNMENT's

Response |

| |

President

of India has finally done it. The Govt has notified the Recruitment Rules

for Chairmen and Members of both the Revenue Boards broadly along the

lines suggested by TIOL experts.SEE

the NEWS |

|

TIOL's

News |

| |

ON January 01, we reported about CBEC’s fiasco on extension of two

CCs'.

SEE

the INSIDER |

| |

|

|

GOVERNMENT's

Response |

| |

After

our news FM himself took action SEE

the RAISINA |

|

TIOL's

News |

| |

AS earlier expressed and being the first to publish 'THE TAXATION LAWS (AMENDMENT)

BILL, 2005', the TIOL team extensively commented on the various proposed

provisions of the Tax Laws

SEE

the BILL |

| |

|

|

PARLIAMENT's

Response |

| |

The STANDING COMMITTEE OF FINANCE BRANCH has asked our Panel of Experts for

valuation views and suggestions on the provisions of the Bill in the form

of a memorandum - LOK

SABHA LETTER dated September 8, 2005 |

|

TIOL's

News |

| |

ON July 01, 2005 we carried our DDT 'Help

Please!' we commented on "cumersome procedure adopted by DGST

for centralised registration of assessees located in the jurisdiction

of more than one Chief Commissioner. " Also it was questioned, "And,

is there any time frame for the registration process to be completed?"

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

The

CBEC conceded our points and has issued instructions overruling DGST and

simplifying the procedure. - CBEC

letter in F.No.354/106/2005-TRU dated 8.8.2005

READ

the DDT |

|

TIOL's

News |

| |

ON August 11, 2005 we carried our DDT 'Finally,

adjudication powers notified for service tax' we talked about "in

the entire 38 paragraphs, nowhere any clarification was found on the issue

of who has to issue and adjudicate show cause notices." Also in earlier

DDT dated July 29, 2005 'Service

tax on new services : TRU issues clarification but only for field'

we pointed out that "mega exercise of budget Notifications, the Board

forgot to specify the powers of adjudication by a Notification under Section

83 A". |

| |

|

|

GOVERNMENT's

Response |

| |

A

notification was issued on August 10, 2005 under Section 83 A of the Finance

Act 1994 prescribing the monetary limits for adjudication of Service Tax

Cases. The powers of AC/JC/ADC/Commissioner are identical to those under

the Central Excise. - Notification

No 30/2005 Service Tax |

|

TIOL's

News |

| |

ON 10th-April-2005, S Jaikumar, G Natarajan & M Karthikeyan our special Guest

reported "DGST floats a new speed breaker for 75 per cent service tax

abatement on GTA!", under which DGST clarified that the benefit of

Notification 32/2004 ST Dated 03.12.2004 (Grant of abatement of 75 % for

the purpose of levy of service tax on GTA services), is applicable only

when the transport agencies pay the service tax and not when the consignor

or the consignee pays the service tax

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

DG

Service Tax has withdrawn the controversial clarification we reported

on 10th April 2005, Now the consignors/consignees can continue to pay

Service Tax on 25% of the value.

READ

the DDT |

|

TIOL's

News |

| |

ON 06.09.2004, in Oil and Power News under 'News Channel' under the story

"NO MORE WAREHOUSING OF PETRO GOODS! CBEC NOT IN HARMONY WITH RULES!",

we had pointed out Since the facility of warehousing has been withdrawn

from 6.9.2004, the excise duty has to be paid by the refineries at the

time of removal from the refineries. But the duty has to be paid only

as per the provisions of Rule 8 of the central excise Rules according

to which the duty for the clearances for the month of September can be

paid by 5th of October 2004.

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Board

clarified vide Circular

No.804/1/2005-CX 4th January, 2005. The attention is invited to

para 1(ii) in Circular

No. 796/29/2004 CX dated 4.9.2004 which stated that as on

or after 6.9.2004, no stocks could remain bonded/ warehoused, the excise

duty on the stocks of petroleum products lying in the warehouses on the

mid night of 5th/6th September 2004 should be paid immediately. The matter

has been re-examined in the light of the representations received in this

behalf. Accordingly, para 1(ii) in the Board's Circular dated 4.9.2004

is clarified to the effect that duty on bonded/warehoused goods (treated

as cleared immediately after 5th/6th September, 2004) could be discharged

in terms of provisions of Rule 8 of Central Excise Rules 2002 i.e. by

5th October, 2004. |

|

TIOL's

News |

| |

ON 19.1.2005, we carried a report about a guitar gifted by an Englishman

to a poor boy in Assam, getting stuck in Kolkotta Customs as none of the

parties concerned, donor, donee or the church through which the gift was

arranged could not afford to pay the 40,000 rupees customs duty. We had

carried the letter from the British donor and requested the Finance Minister

to help.

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

(F.No.401/6/2005-Cus.III) See the full text of the Board’s letter to us. |

|

TIOL's

News |

| |

TIOL sensitises Govt about circular trading in precious metals; DGFT prescribes

higher value addition norms and calls for a match for forex outgo

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Government

has finally worked out an effective way out. Instead of using the RBI instrument

the Govt asked the DGFT to prescribe a higher value addition formula for

exports of studded jewellery (DGFT

Cir No.18/2004-09)

See

related STORY. |

|

TIOL's

News |

| |

Taxindiaonline had carried an article "CESTAT, Chennai joins FM in his revenue drive!".

The article had pointed out that the Chennai bench of the CESTAT has recently

insisted that a fee of Rs. 500/- should be paid even for adjournments

in the Tribunal. The article had pointed out that sometimes adjournments

are sought mid way through the arguments and at that point of time it

would be difficult to get a draft for Rs. 500/

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Tribunal has

clarified that there is no fee for adjournments in the Tribunal. In CESTAT

Public Notice No. 1/2005, the Vice President Ms Jyoti Balasundaram has clarified

that requests for adjournments are not considered to be formal applications

and so no fee is required to be paid. (CESTAT

PN No. 1/2005)

See

the STORY. |

|

TIOL's

News |

| |

ON August 11, 2005 we carried our DDT 'Finally,

adjudication powers notified for service tax' we talked about "in

the entire 38 paragraphs, nowhere any clarification was found on the issue

of who has to issue and adjudicate show cause notices." Also in earlier

DDT dated July 29, 2005 'Service

tax on new services : TRU issues clarification but only for field' we

pointed out that "mega exercise of budget Notifications, the Board forgot

to specify the powers of adjudication by a Notification under Section 83

A". |

| |

|

|

GOVERNMENT's

Response |

| |

A notification

was issued on August 10, 2005 under Section 83 A of the Finance Act 1994

prescribing the monetary limits for adjudication of Service Tax Cases. The

powers of AC/JC/ADC/Commissioner are identical to those under the Central

Excise. - Notification

No 30/2005 Service Tax |

|

TIOL's

News |

| |

ON 10th-April-2005, S Jaikumar, G Natarajan & M Karthikeyan our special Guest

reported "DGST floats a new speed breaker for 75 per cent service tax

abatement on GTA!", under which DGST clarified that the benefit of

Notification 32/2004 ST Dated 03.12.2004 (Grant of abatement of 75 % for

the purpose of levy of service tax on GTA services), is applicable only

when the transport agencies pay the service tax and not when the consignor

or the consignee pays the service tax

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

DG

Service Tax has withdrawn the controversial clarification we reported on

10th April 2005, Now the consignors/consignees can continue to pay Service

Tax on 25% of the value.

READ

the DDT |

|

TIOL's

News |

| |

ON 06.09.2004, in Oil and Power News under 'News Channel' under the story

"NO MORE WAREHOUSING OF PETRO GOODS! CBEC NOT IN HARMONY WITH RULES!",

we had pointed out Since the facility of warehousing has been withdrawn

from 6.9.2004, the excise duty has to be paid by the refineries at the

time of removal from the refineries. But the duty has to be paid only

as per the provisions of Rule 8 of the central excise Rules according

to which the duty for the clearances for the month of September can be

paid by 5th of October 2004.

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Board

clarified vide Circular

No.804/1/2005-CX 4th January, 2005. The attention is invited to

para 1(ii) in Circular

No. 796/29/2004 CX dated 4.9.2004 which stated that as on or

after 6.9.2004, no stocks could remain bonded/ warehoused, the excise duty

on the stocks of petroleum products lying in the warehouses on the mid night

of 5th/6th September 2004 should be paid immediately. The matter has been

re-examined in the light of the representations received in this behalf.

Accordingly, para 1(ii) in the Board’s Circular dated 4.9.2004 is clarified

to the effect that duty on bonded/warehoused goods (treated as cleared immediately

after 5th/6th September, 2004) could be discharged in terms of provisions

of Rule 8 of Central Excise Rules 2002 i.e. by 5th October, 2004 . |

|

TIOL's

News |

| |

ON 19.1.2005, we carried a report about a guitar gifted by an Englishman

to a poor boy in Assam, getting stuck in Kolkotta Customs as none of the

parties concerned, donor, donee or the church through which the gift was

arranged could not afford to pay the 40,000 rupees customs duty. We had

carried the letter from the British donor and requested the Finance Minister

to help.

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

(F.No.401/6/2005-Cus.III) See the full text of the Board’s letter to us. |

|

TIOL's

News |

| |

TIOL sensitises Govt about circular trading in precious metals; DGFT prescribes

higher value addition norms and calls for a match for forex outgo

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Government

has finally worked out an effective way out. Instead of using the RBI instrument

the Govt asked the DGFT to prescribe a higher value addition formula for

exports of studded jewellery (DGFT

Cir No.18/2004-09)

See

related STORY. |

|

TIOL's

News |

| |

Taxindiaonline had carried an article "CESTAT, Chennai joins FM in his revenue drive!".

The article had pointed out that the Chennai bench of the CESTAT has recently

insisted that a fee of Rs. 500/- should be paid even for adjournments

in the Tribunal. The article had pointed out that sometimes adjournments

are sought mid way through the arguments and at that point of time it

would be difficult to get a draft for Rs. 500/

READ

the ARTICLE |

| |

|

|

GOVERNMENT's

Response |

| |

Tribunal has

clarified that there is no fee for adjournments in the Tribunal. In CESTAT

Public Notice No. 1/2005, the Vice President Ms Jyoti Balasundaram has clarified

that requests for adjournments are not considered to be formal applications

and so no fee is required to be paid. (CESTAT

PN No. 1/2005)

See

the STORY. |

|