TIOL-DDT 2948 TIOL-DDT 2948

13 10 2016

Thursday

AS per Article 279A of the Constitution of India, the President shall constitute the GST Council which shall make recommendations to the Union and States on the items specified under sub-clause (a) to (h) of clause (4).

As per clause (9), every decision of the GST Council shall be taken at a meeting, by a majority of not less than three fourths of the weighted votes of the members present and voting in accordance with the following principles:

(a) the vote of the Central Government shall have a weightage of one third of the total votes cast, and

(b) the votes of all the State Governments taken together shall have a weightage of two-thirds of the total votes cast, in that meeting.

This weighted vote system has been illustrated in the Statement of Objects and Reasons of the Bill as under:

Illustration:

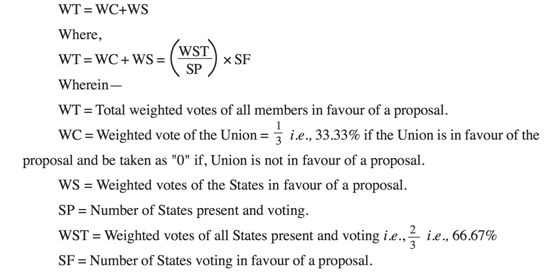

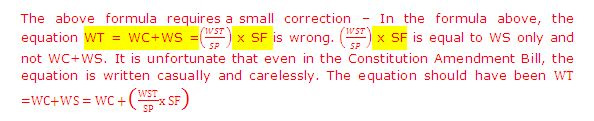

In terms of clause (9) of the proposed article 279A, the "weighted votes of the members present and voting" in favour of a proposal in the Goods and Services Tax Council shall be determined as under: -

If all States present, vote in favour of a proposal and the Centre also supports it, then there is no problem as the total percentage will be - 33.3 ( WC) + 66.7 (WS) = 100%

If all States decide that the RNR should be say 18% and if the Centre does not agree with it, the proposal fails as it gets only 66.67% as against minimum majority of 3/4th or 75%. [0+2/3 x 31/31 = 2/3=66.67%, if 31 States attend and vote.)

Similarly, if Centre wants to impose RNR of 20% and if all the States oppose it, then it will not be passed with 33.3% in favour and 66.7% against. [1/3+2/3 x 0/31 = 1/3 = 33.33%]

Thus, both Centre and States should work together and each cannot unilaterally decide on any issue.

What happens if the States are divided among themselves in respect of a proposal? What is the minimum number of States required to vote in favour of any proposal?

Let us examine. If out of 31 States, 20 States vote in favour, then the WS =  43% 43%

Now, WT = WC + WS = 33 + 43 = 76% > 75% - The proposal will pass.

Thus, the Centre, in addition to 33.33%, needs a minimum 41.67% from the States' share as WS. Since the States' weighted vote is taken as 66.67% only, the SF/SP ratio should not be less than 62.5% to achieve this 41.67%

Since the quorum required is 50%, assuming minimum 16 States present and participate in voting, for any proposal to pass, at least 62.5% of 16 States, i.e, 10 Members should vote in favour.

On the other hand, if the States want to exercise a kind of VETO (Assuming the scenario where opposition States vote against and ruling party States vote in favour), minimum votes required against the proposal is:

31 x (100-62.5) = 31 x 37.5% = 12.

So, out of 31, if 12 States oppose, a proposal will not get the required majority of 75% or 3/4th.

Maybe along with the CBEC Chairperson, they should make a statistician a permanent invitee to all the meetings of the GST Council to calculate and report the result of voting.

GST - From Consensus to Voting - Cooperative Federalism at Work?

AS per the present constitution, decisions of the GST Council will need support of 3/4th of the weighted votes. This was not as originally proposed. In the Constitution (115th Amendment) Bill presented to Lok Sabha in 2011 provided for a consensus and not voting. Article 279A(8) proposed;

Every decision of the Goods and Services Tax Council taken at a meeting shall be with the consensus of all the members present at the meeting.

So, unanimity was constitutionally sought to be mandated. But the Select Committee, to which the Bill was referred, observed,

9. The Committee note that the decisions in the GST Council, would be taken, based on consensus which implies that all the members present would have to agree to a proposal; even if one State differs, the decision cannot be passed. The Committee feel that keeping in view the diversity in socio-economic interests of the States, achieving such a consensus is likely to be very difficult. As it would be critical in ensuring that all the valid interests are properly reflected in the recommendations of the GST Council, the Committee would therefore recommend amendments to Clause (8) of Article 279A so as to provide for voting instead of consensus for decisions of the GST Council. Accordingly, as agreed upon by the Empowered Committee, one-third weightage for central representatives and two-thirds weightage for state representatives may be provided with the decision taken by the Council being passed with more than three fourths votes of the representatives present in the meeting. Similarly, amendment to Clause (6) of Article 279A may also be made for increasing the quorum to half from the proposed one-third. In this context, the Committee would recommend that in tune with the spirit of cooperative federalism, it would be in order if the proposed GST Council functions like the present Empowered Committee, which has had a good track record of not only reforming the tax system but also resolving differences amicably in an institutional mode.

That is how the complicated looking formula got into GST!

GST - How Many Votes Will Centre Have?

AS per Article 279A(2), the Goods and Services Tax Council shall consist of the following members, namely:-

|

a.

|

the Union Finance Minister........................

|

Chairperson;

|

|

b.

|

the Union Minister of State in charge of Revenue or Finance............................

|

Member;

|

|

c.

|

the Minister in charge of Finance or Taxation or any other Minister nominated by each State Government...............

|

Members.

|

Now, the Union Finance Minister and the Minister of State for Finance are Members of the GST Council and are there by a Constitutional mandate, each by his individual designation. But then will each of them have a separate vote to calculate the Centre's one third votes and if so, what happens if they vote differently - one for and one against? If there is only one vote, who will vote? The Finance Minister or his deputy? Can the Minister of State be barred from voting? This is the first time that a Minister by his portfolio is mentioned in the Constitution and if they want to change that, they will have to amend the Constitution. Maybe it is not wise to mention every detail in the Constitution.

We are not Criticising Government - IRS Association

THE CBEC in a letter dated 29.09.2016, had observed,

Of late, it has been noticed that some Associations/Federations have commented adversely on the Government and its policies. It may be brought to the notice of all Associations/Federations that if anyone indulges in criticism of the Government and its policies, appropriate action (including disciplinary action) shall be taken under Rule 9 of the Central Civil Services (Conduct) Rules, 1964. (Please see Don't Criticise Govt. - CBEC Tells Staff Associations - DDT 2941).

Perhaps to clarify its position, the IRS (C&CE) Association in a Resolution dated 06.10.2016 states:

1. IRS (C&CE) officers as well as Association are totally committed to very successful and smooth implementation of GST in the country w.e.f. 1st April, 2017.

2. Association has never ever opposed any decisions of the government nor intends to do so.

3. The representations made to Hon'ble Finance Minister are legitimate and the association will continue to take up the genuine concerns with the competent authorities appropriately.

4. CBEC& IRS officers have requisite experience of working smoothly and successfully in the field of Indirect Tax Administration in the country for decades and have witnessed several transitions without any glitch including when first time Service Tax was implemented in India in 1994.

5. At the moment, we assure one and all that we are for extremely successful implementation of GST and ready to do whatever is required. However, the State VAT officials may not be allowed to bring distortions in GST to weaken the Centre. A strong sustainable Centre is the need of the hour.

While the commitment and promise of the association are laudable what makes them think that the State VAT officials will bring distortions in GST to weaken the Centre? After all, the senior officers of the VAT in the States are officers of “All India Service" called the IAS, to which their illustrious boss, the Revenue Secretary also belongs. Further what does it mean by A strong sustainable Centre is the need of the hour ? Don't we have one already?

I tried to contact the Association by mail and phone but couldn't get a response.

CBEC to Meet Associations on GST Today

IT is learnt that CBEC has called for a meeting of the Steering Committee of Associations in CBEC today at 04.00 pm to be chaired by Member (Admn), to discuss issues relating to GST.

Voluntary Retirement Application of Commissioner Rejected for not Stating Rule

A Principal Commissioner of Income Tax by his letter dated 11.07.2016 submitted a notice seeking voluntary retirement from Government Service. This was forwarded by the Principal CCIT to the Board in his undated letter. This was received in the Board on 09.08.2016. Maybe he should have retired on 10.10.2016 on which date, the CBDT communicated to him that the President of India is pleased to reject his voluntary retirement as the notice given by him is defective inasmuch as he has not indicated the Rule under which he is seeking voluntary retirement !

A Government Servant is covered under various Rules in respect of Voluntary retirement.

As per Fundamental Rule (FR) 56(k), Group A and B officers who have entered service before 35 years of age and attained 50 years of age, can retire on a notice of three months.

As per Rule 48(1)(a), a government servant with a service of 30 years can seek voluntary retirement.

As per Rule 48(A), a Government with a service of 20 years can seek voluntary retirement.

The CBEC had in May 2016 issued detailed guidelines along with a form for voluntary retirement. (DDT 2837) and one of the fields to be filled up is the Rule under which VRS is sought.

In this case the application for VRS was from a senior officer of the rank of PC. The application was scrutinised by a Principal CC and the Board and is rejected at the end of the notice period. At any stage, it could have been corrected. It is doubtful whether all the officers who have taken VRS so far have mentioned the correct rule or for that matter any rule under which they sought VRS.

Government is government even for a babu!

CBDT No. A-38012/19/2016-AdVI(A)., Dated: October 10 2016

26% Increase in Indirect Taxes Collection

THE figures for indirect tax collections (Central Excise, Service Tax and Customs) up to September 2016 show that net revenue collections are at Rs 4.08 lakh crore which is 25.9% more than the net collections for the corresponding period last year. Till September 2016, 52.5% of the Budget Estimates of indirect taxes for Financial Year 2016-17 has been achieved.

As regards Central Excise, net tax collections stood at Rs.1.83 lakh crore during April-September, 2016 as compared to Rs.1.25 lakh crore during the corresponding period in the previous Financial Year, thereby registering a growth of 46.3%.

Net Tax collections on account of Service Tax during April-September, 2016 stood at Rs.1,16,975 crore as compared to Rs. 95,780 crore during the corresponding period in the previous Financial Year, thereby registering a growth of 22.1%.

Net Tax collections on account of Customs during April-September 2016 stood at Rs. 1.08 lakh crore as compared to Rs. 1.03 lakh crore during the same period in the previous Financial Year,thereby registering a growth of 4.8%.

Direct Tax Collections upto Sep,16 up by 8.95%,with net collection of Rs3.27lakh crore. Growth rate for Corporate Income Tax (CIT) is 9.54% while that for Personal Income Tax (PIT) is 16.85% in terms of gross revenue collections. Refunds amounting to Rs.86,491 crore have been issued during Apr-Sep 2016, which is 26.99% higher than the corresponding period last year.

Taxation is transactional and not cuneiform.

|

Until Tomorrow with more DDT

Have a nice day.

Mail your comments to vijaywrite@tiol.in |

Download PDF

Download PDF